Understanding how VCs actually think about funding your startup reveals a philosophy called the Greater Fool Theory that drives much of early stage venture capital decision-making. If you're raising venture capital, you need to understand that for most VCs, funding decisions are primarily about whether you will raise the next round at a higher valuation, not whether your business is fundamentally sound or sustainable. This approach to venture capital means that as long as the VC believes you can find other investors willing to pay more for your shares down the road, they're safe because you become somebody else's problem. The Greater Fool Theory often leads to dumb money decisions and inflated valuations like WeWork and Clubhouse because it works until suddenly no one will pay higher valuations. Understanding this dynamic helps founders navigate fundraising reality and recognize when they're building on fundamentals versus momentum.

What VCs Really Care About

For most VCs, it is about whether you will raise the next round. Are you capable of raising the next round? This is particularly true in early stage and that too not just if you will raise your next round, whether you are capable of raising your next round at a higher valuation.

Most early stage funds are not really very big funds, so it's critical for them that you go on to raise a bigger round from somebody who has deeper pockets. Because they will not be able to really support you by themselves down the road even if you're growing because their fund is not that large.

This reality shapes every interaction you have with early stage VCs. They're not just evaluating your business. They're evaluating whether Series A or Series B funds will want to invest in you later. Your ability to attract future capital matters more than your current metrics.

The Greater Fool Theory Explained

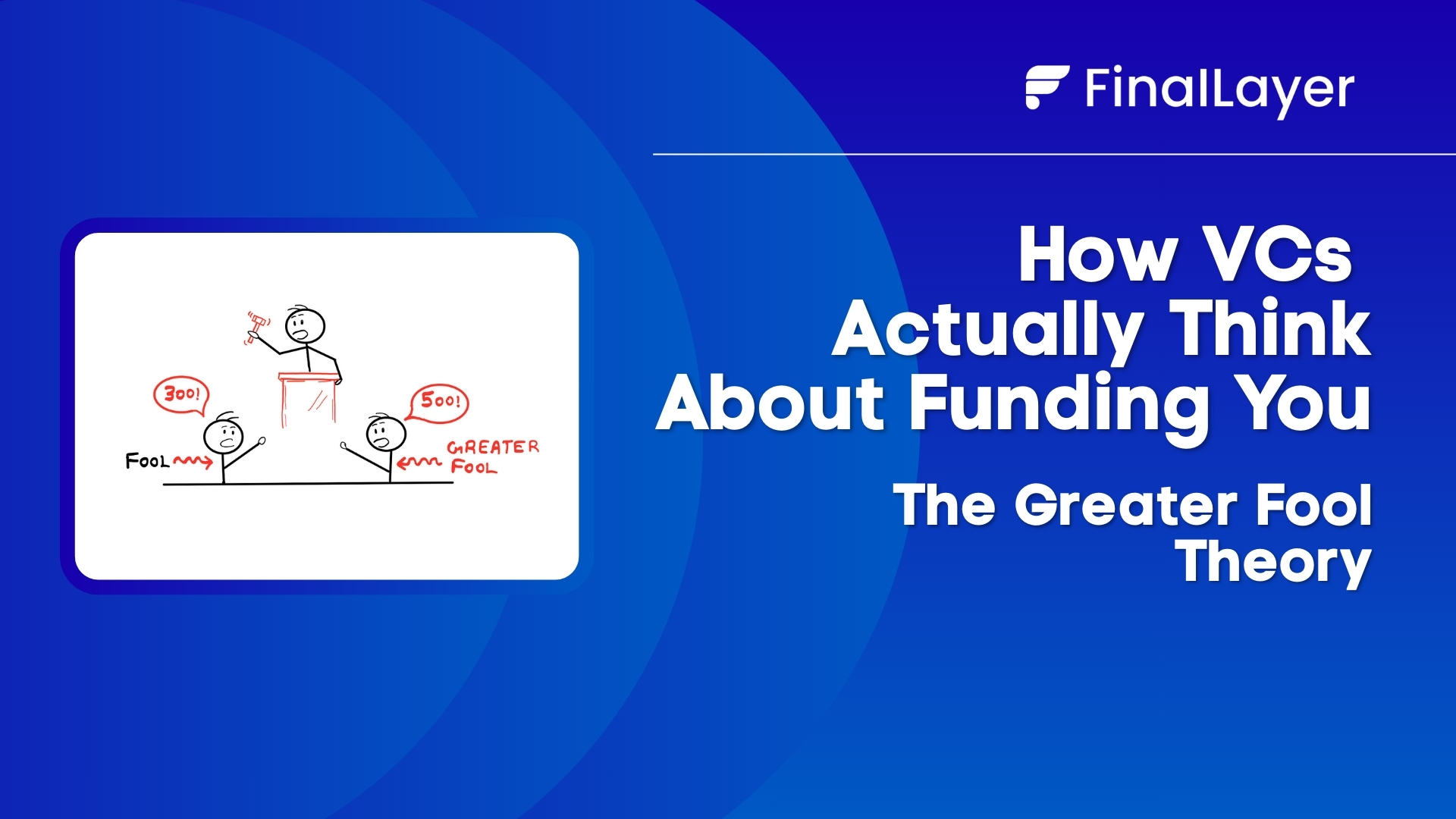

This often leads to what is called the Greater Fool Theory in economics.

The Greater Fool Theory basically says as long as you can find other investors who are willing to pay more for your shares down the road, that particular investor is safe because now you are somebody else's problem. Greater Fool Theory often leads to very dumb money in venture capital. It often leads to very bad decisions.

Because this theory just works until it doesn't, until you can no longer find investors who are willing to pay into your company higher valuations than what you had before. But a lot of early stage venture capital still works on the Greater Fool Theory philosophy.

Understanding the difference between smart money and dumb money becomes critical here, as Greater Fool Theory investing represents a classic form of dumb money that prioritizes exit opportunities over company fundamentals.

When the Theory Breaks Down

Mistakes like WeWork happen because this theory is really stretched to the fringes in cases like that. WeWork raised billions at increasingly absurd valuations because each round of investors believed the next round would pay even more. Until suddenly, no one would.

The music stops when market conditions change, when your metrics don't support the narrative anymore, or when the valuation becomes so disconnected from reality that even momentum-driven investors won't participate.

How Smart VCs Weaponize the Theory

Also some smarter VCs will inflate the valuations of their portfolio companies in order to accelerate the Greater Fool Theory and attract more capital. Classic example is A16Z. For example, A16Z led multiple rounds of funding in Clubhouse.

They raised in May 2020, they raised a Series A for $10 million. Then they raised $100 million at a billion dollar valuation just eight months after that in January 2021. And just three months after that, they raised around for $4 billion valuation which had participation from DST Global and Tiger Global, two other giants other than A16Z.

By creating that insane momentum, they were able to draw in two other global VCs into the cap table so that they will have more firepower when they scale down the road. This is a playbook that has often worked for A16Z, but in this particular case with Clubhouse, even that couldn't solve it.

The Momentum Play

The strategy is brilliant in its cynicism. Raise at $10M valuation, then 8 months later raise at $1B (100x jump), then 3 months later raise at $4B. Each round creates FOMO (fear of missing out) for the next round of investors.

By the time Tiger Global and DST Global invested at $4B valuation, they weren't investing based on fundamentals. They were investing based on momentum and the belief that A16Z's track record meant this would work out somehow.

When you're pitching to investors, understanding these dynamics helps you recognize when VCs are making Greater Fool Theory bets versus genuine belief in your business model.

Why This Matters for Founders

Understanding the Greater Fool Theory changes how you think about fundraising:

First, recognize that early stage VCs are often not investing in your business per se. They're investing in your ability to attract the next round. This means your narrative, momentum, and network matter as much as your metrics.

Second, understand that inflated valuations can backfire. If you raise at $50M valuation when you should have raised at $20M, you've created a trap. Your next round needs to be at $150M+ or you'll face a down round, which scares investors away.

Third, the Greater Fool Theory works brilliantly in hot markets and fails spectacularly in cold ones. When capital is abundant and valuations are rising across the board, everyone can find a greater fool. When markets turn, you're left holding an inflated valuation with no path to your next round.

This connects directly to whether you should raise VC money at all. If you're going to play the venture capital game, understand that you're playing a game of musical chairs where the music can stop at any time.

The Alternative Approach

Not all VCs operate on Greater Fool Theory. Some genuinely evaluate business fundamentals, unit economics, and sustainable growth. These investors are harder to find but more valuable when markets turn.

The question becomes: do you want investors who believe in your business, or investors who believe in their ability to find someone else to pay more? The answer affects everything from your exit strategy to how you structure your cap table.

When considering whether to become a founder in the VC-backed startup world, understanding these dynamics helps you make informed decisions about whether this game is one you want to play.

Lessons for Building FinalLayer

At FinalLayer, we're building with these lessons in mind. We understand the Greater Fool Theory dynamics but choose to focus on fundamentals: real users, real value creation, and sustainable unit economics.

While some companies chase inflated valuations and momentum-driven funding rounds, we're focused on building a business that doesn't depend on finding a greater fool. Sometimes the smartest play is refusing to play the game at all.

If you're navigating VC funding decisions and want to discuss these dynamics with other founders, join our founder's Slack community where we share experiences about fundraising strategies, investor dynamics, and building sustainable companies in the Founder Resources tab.