Credit card industry

The credit card industry encompasses a comprehensive network of financial products and services that significantly influence consumer spending behavior and the overall economy. As of recent reports, there are over 800 million active credit cards in the U.S., with approximately 82% of adults holding at least one card. Credit card payments account for about 31% of all transactions nationally, indicating their central role in facilitating everyday purchases, including essential goods and services, travel, and online shopping. With a staggering total revolving debt reaching around $1.18 trillion, understanding the dynamics of credit card usage, debt management, and consumer preferences is essential for both consumers and financial institutions. In recent years, the industry has seen transformations driven by advancements in digital payments, particularly the rise of contactless methods and mobile wallets such as Apple Pay and Google Pay. Coupled with enhancements in credit card rewards programs, these developments are reshaping consumer behavior, with many favoring cards for their flexible repayment options and reward opportunities. However, challenges continue to arise, including increased credit card delinquency rates, particularly among younger populations, and the tension created by rising interest rates, which average around 21.6% across various cards. As the credit card landscape evolves, it remains critical for consumers to navigate this complex financial ecosystem with awareness of both the opportunities and the risks associated with credit card adoption and usage.

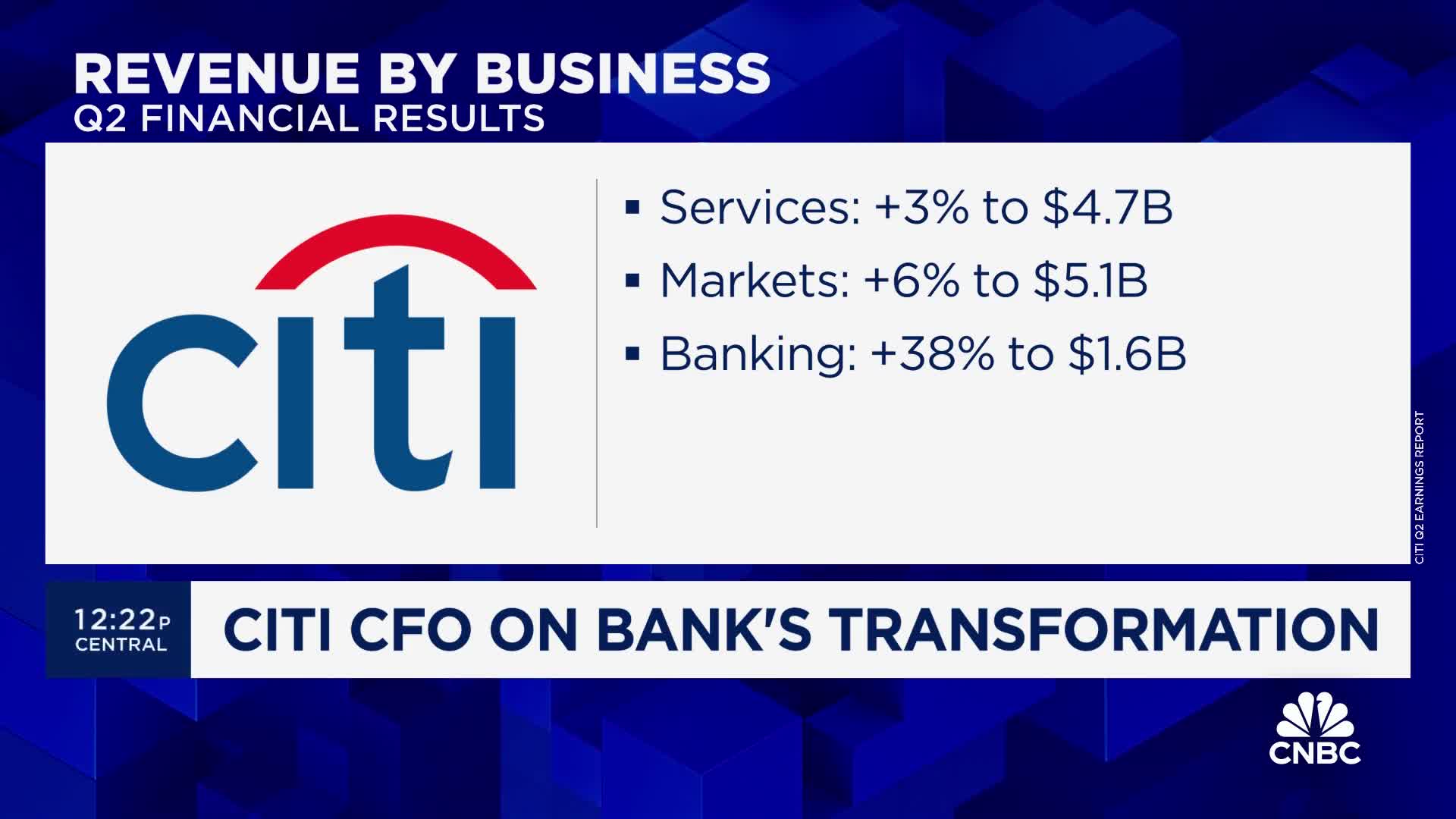

Is Citigroup adequately provisioned for an economic slowdown?

According to Mark Mason, Citigroup is well-provisioned for virtually any economic scenario with over $22 billion in reserves against their loans, representing a 2.7-2.8% funded loan ratio. Their stress scenarios incorporate various economic conditions, including a base case assuming 5% unemployment and downside scenarios with 6.8% unemployment. While consumer credit losses have increased as part of expected normalization, corporate losses remain minimal due to their high-quality corporate loan book. Mason noted an interesting dichotomy in consumer behavior, with higher FICO score customers increasing spending while lower FICO consumers are reducing payment rates and increasing borrowing activity.

Watch clip answer (02:48m)

CNBC Television

03:37 - 06:26

What is the significance of the Capital One and Discover merger?

The merger represents a significant consolidation in the financial sector, with shareholders recently approving a $35 billion deal between Capital One and Discover. Upon completion, this strategic combination will transform Capital One into the largest credit card issuer in the United States, marking a pivotal shift in the credit card industry landscape. This development is noteworthy not just for the companies involved but potentially for consumers as well. As the merged entity gains increased market share and greater economies of scale, it may lead to expanded payment access options and possibly lower interest rates for credit card users.

Watch clip answer (00:12m)

CBS News

42:01 - 42:14

What is the current threat level of an asteroid hitting Earth?

NASA astronomers are tracking a large asteroid (130-300 feet long) expected to pass close to Earth in December 2032. The probability of impact has increased to just over 3%, up from 2.8% previously. This represents the highest risk level ever recorded for a large space rock. Despite this increase, the overall odds remain relatively low, and experts advise the public to remain calm about the potential threat.

Watch clip answer (01:08m)

CBS News

41:48 - 42:56

What are the key details and potential impacts of the Capital One and Discover merger?

Shareholders have approved a $35 billion merger between Capital One and Discover, which would make Capital One the largest credit card issuer in the United States. This significant consolidation in the financial services industry represents a strategic move to enhance Capital One's market position. According to experts, the merger could deliver several consumer benefits, including expanded payment access locations where customers can use their cards. Additionally, the combined entity may potentially offer lower interest rates to consumers, making credit more affordable. The deal marks a major shift in the credit card landscape that could reshape competition in the industry.

Watch clip answer (00:16m)CBS News

42:01 - 42:18

What would be the outcome of the potential merger between Capital One and Discover?

The merger would establish Capital One as the largest credit card issuer in the United States, surpassing JPMorgan Chase. This significant consolidation in the credit card industry was announced about a year ago, but still requires full federal regulatory approval before it can be finalized. Currently, shareholders of both companies are voting on this potential merger, which represents a major shift in the competitive landscape of credit card companies. If approved, the deal would reshape the hierarchy of credit card issuers in the American financial market.

Watch clip answer (00:16m)

CBS News

00:05 - 00:21

What would the Capital One and Discover merger mean for the credit card industry and consumers?

The merger would create scale and cost synergies, propelling Capital One to become the largest credit card issuer in the U.S. By acquiring Discover's payment network infrastructure, Capital One would reduce dependency on Visa and MasterCard, allowing them to better compete with these dominant players who control 76% of the market. For consumers, benefits include increased access to ATM locations and potentially better credit offers with lower rates. However, some analysts caution that reduced competition from consolidation could potentially have negative impacts, which is why regulatory approval remains a key hurdle for this significant industry transformation.

Watch clip answer (01:21m)CBS News

00:34 - 01:56